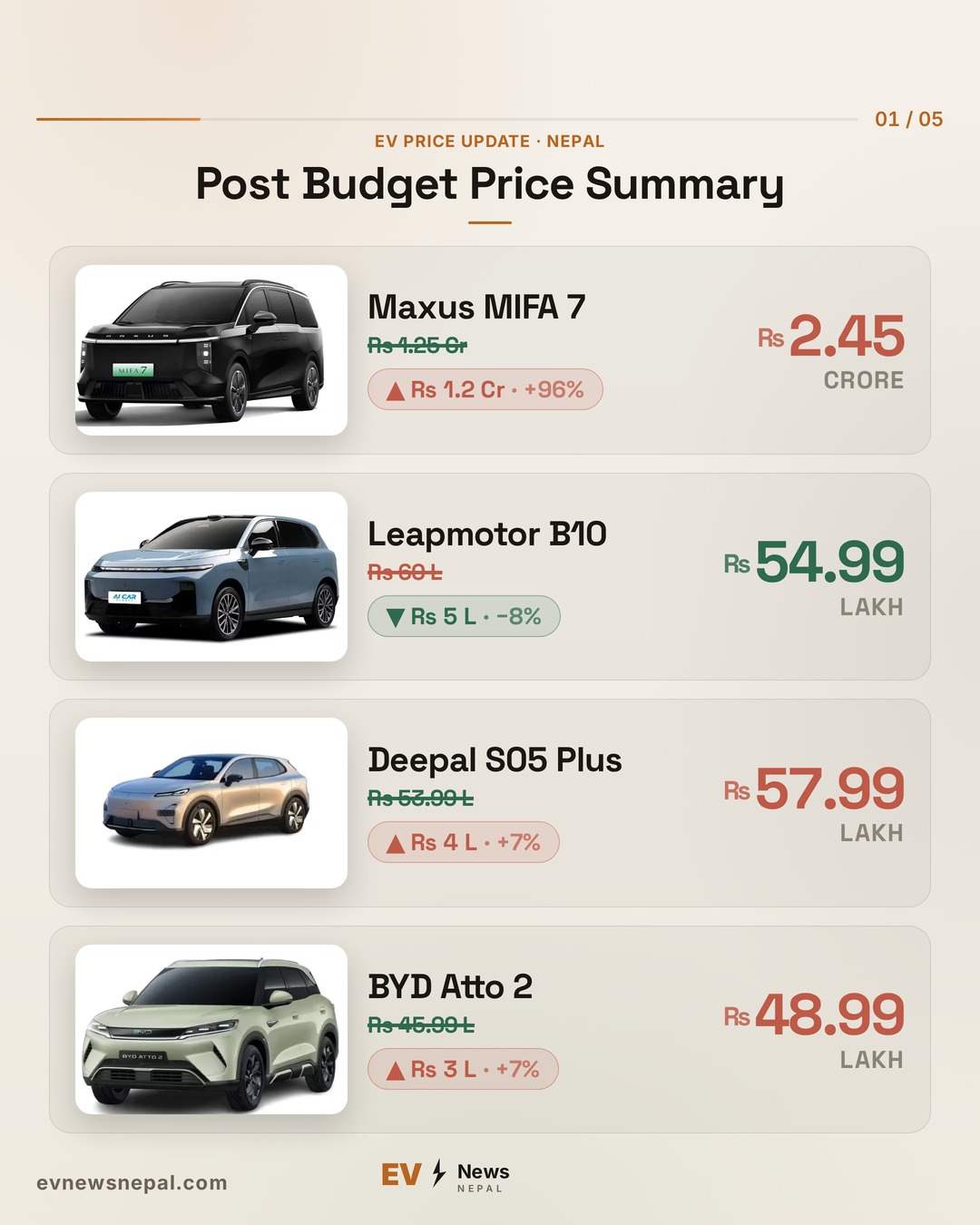

Nepal EV Tax Changes Impact on Vehicle Prices Explained Clearly

AI illustration

AI illustrationKey Takeaways

- Nepal's new EV tax system replaces kW-based levies with CIF value-based taxation, increasing costs for mid-range and premium models

- Vehicles under Rs 20 lakh CIF face a 28.5% total tax burden, while those above Rs 50 lakh incur up to 130% levies

- Exchange rate fluctuations could push vehicles between tax brackets, creating pricing instability for importers and buyers

- The Clean Infrastructure Investment Tax aims to fund charging networks and battery recycling but may raise showroom prices

- Lower-cost EVs may see minimal price changes, while higher-value electric vehicles face significant cost increases

New EV Taxation System Sparks Debate in Nepal

Government Introduces Value-Based Taxation for Electric Vehicles

Nepal’s new electric vehicle (EV) taxation system has generated significant discussion among consumers and industry stakeholders. The revised structure, which replaces the previous power-based taxation model, now uses the Cost, Insurance, and Freight (CIF) value to determine tax liabilities. This shift directly links taxation to import value rather than technical specifications, meaning vehicle price has become the key determinant of tax burden.

Key Changes in EV Taxation

Under the previous system, EV taxes were primarily determined by motor power measured in kilowatts (kW). The new budget replaces this with a value-based approach, calculating taxes on the CIF value—which includes the vehicle’s cost, insurance, and freight up to Nepal’s border.

For EVs with a CIF value up to Rs 20 lakh, the tax structure includes:

- 20% customs duty

- 2.5% Clean Infrastructure Investment Tax (calculated on CIF plus customs duty)

- Road Development Fee: 2.5% for EVs below Rs 50 lakh and 5% above that threshold

- 13% VAT applied at the final stage

These components combine to form the total government-imposed tax burden on EV imports. The tax calculation follows this sequence: CIF Value → Customs Duty → Clean Infrastructure Tax → Road Development Fee → VAT → Final Taxable Value.

Tax Calculation Example

Consider an EV with a CIF value of Rs 20 lakh:

| Step | Component | Calculation | Amount (Rs) | Running Total (Rs) |

|---|---|---|---|---|

| 1 | CIF Value | Base Import Value | 20,00,000 | 20,00,000 |

| 2 | Customs Duty (20%) | 20% of CIF | 4,00,000 | 24,00,000 |

| 3 | Clean Infrastructure Investment Tax (2.5%) | 2.5% of (CIF + Customs Duty) | 60,000 | 24,60,000 |

| 4 | Road Development Fee (2.5%) | 2.5% of step 3 total | 61,500 | 25,21,000 |

| 5 | VAT (13%) | 13% of step 4 | 3,27,730 | 28,48,730 |

It’s important to note this calculation represents only government taxes and duties. It excludes importer or dealer margins, which vary depending on brand, logistics costs, and market strategy.

Higher-Value Vehicles Face Steeper Levies

One significant aspect of the new system is the sharp increase in taxation for higher-value vehicles:

- Rs 20–30 lakh: 20% levy

- Rs 30–40 lakh: 35% levy

- Rs 40–50 lakh: 90% levy

- Above Rs 50 lakh: 130% levy

This progressive structure means lower-priced EVs may see limited pricing changes, while mid-range and premium electric vehicles are more likely to experience noticeable price increases under the revised tax system.

Exchange Rate Volatility Impacts CIF Thresholds

Another critical factor influencing final EV pricing is exchange rate volatility. Since CIF is calculated in foreign currency before conversion into Nepali rupees, fluctuations in the USD exchange rate can significantly alter the final taxable value.

For example, a vehicle priced at USD 15,000:

- At Rs 130 per USD, CIF = Rs 19,50,000 (below Rs 20 lakh threshold, lower tax bracket)

- At Rs 136 per USD, CIF = Rs 20,40,000 (above Rs 20 lakh threshold, higher tax burden)

This means the same vehicle could fall into different tax brackets and end up with different showroom prices solely due to exchange rate movements.

Clean Infrastructure Investment Tax Objectives

The government introduced the Clean Infrastructure Investment Tax to fund charging infrastructure, battery recycling facilities, and broader EV ecosystem development. However, the real-world impact on showroom prices will depend heavily on CIF valuation, importer pricing strategies, and currency fluctuations.

While some lower-cost EVs may maintain relatively stable prices, mid-range and premium models are more likely to face upward pricing pressure under the revised tax structure. Consumers and industry stakeholders will need to carefully monitor these dynamic factors as they shape Nepal’s emerging electric vehicle market.