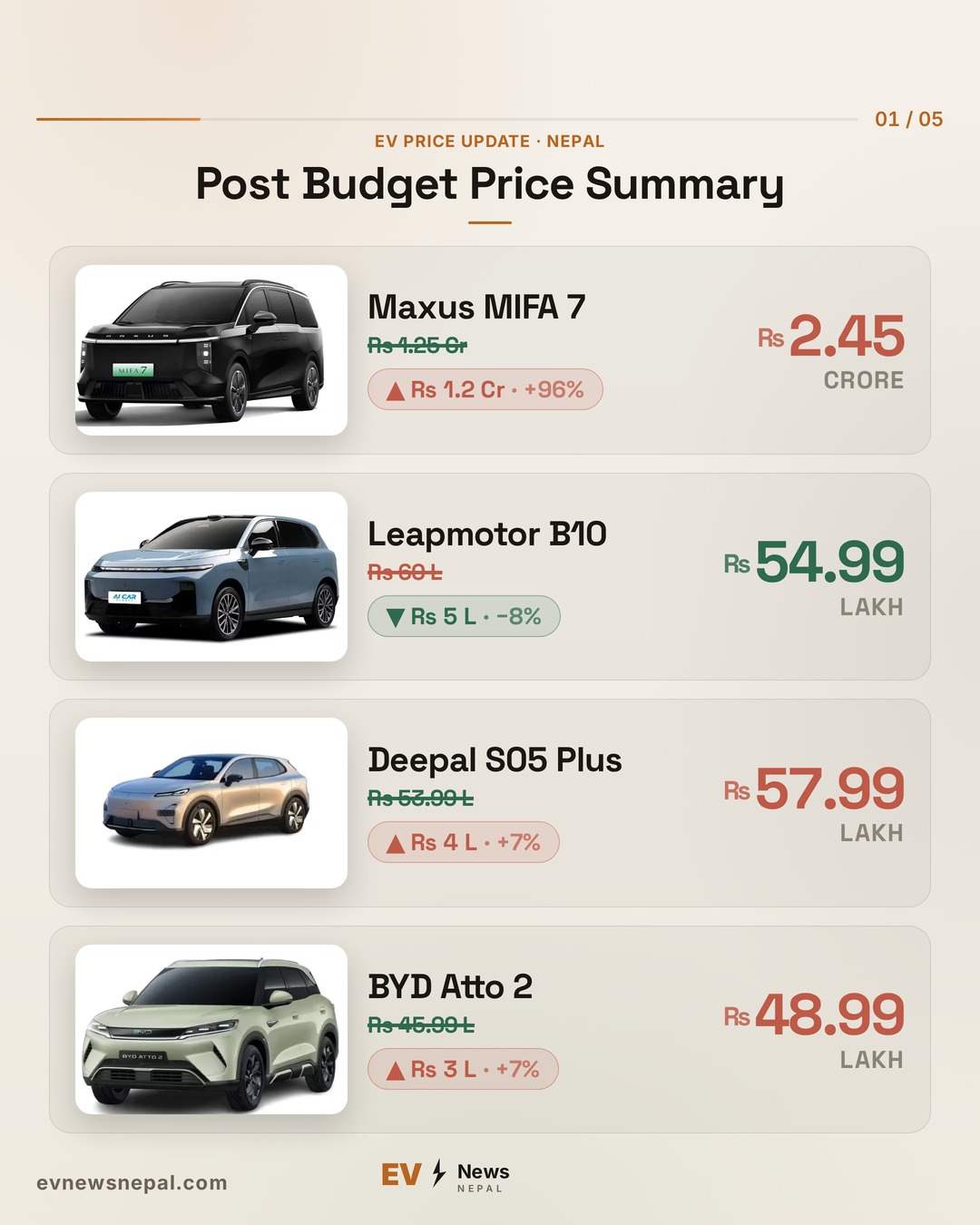

Nepal Shifts EV Tax Structure from Motor Power to Vehicle Price

AI illustration

AI illustrationKey Takeaways

- Nepal's government has shifted EV taxation from a kilowatt-based system to a price-based framework for the fiscal year 2026–27.

- The new policy aims to improve transparency and practicality in the EV tax structure, addressing previous inconsistencies in motor capacity measurements.

- A clean infrastructure investment fee has been introduced on EV imports to support local EV production and the development of charging stations and battery management systems.

New EV Tax System Shifted to Price-Based Model

The government has introduced a major change to the taxation system for electric vehicles (EVs) for the fiscal year 2026–27. Finance Minister Dr. Swornim Wagle announced in the federal parliament that the existing motor power (kilowatt)-based tax structure will be replaced with a new framework based on the vehicle’s purchase price.

Previously, electric vehicles were taxed under a tiered system that relied on motor capacity. This system included five different slabs: 0–50 kW, 51–100 kW, 101–200 kW, 201–300 kW, and any capacity above 300 kW. However, the new policy shifts the focus entirely to the actual market value of the vehicle, moving away from technical motor output as the basis for taxation.

As part of the reform, customs duties on electric vehicles will now be calculated based on the vehicle’s price rather than its peak power capacity. In addition to this change, the government has introduced a clean infrastructure investment fee that applies at the point of import. This fee is designed to encourage local production of electric vehicles and support the development of essential infrastructure such as charging stations and battery management systems.

The decision to overhaul the EV tax system follows years of discussion and evaluation. The Office of the Auditor General previously highlighted issues with the kilowatt-based classification, pointing out inconsistencies and recommending clearer standards for measuring motor capacity. The office also suggested exploring alternative methods, such as value-based taxation, as a more effective solution.

Similar recommendations came from both the Department of Transport Management and the Department of Customs. These departments argued that a system based on vehicle price and size would offer greater transparency and result in a more practical tax structure. After conducting internal assessments and holding high-level discussions within the Ministry of Finance, the government has now officially adopted the price-based taxation model for electric vehicles.